Frequently Asked Questions

What is SBI Life - eShield?

SBI Life - eShield is an individual, Non Linked (Traditional), Non-Participating,

Online pure term plan.

What are the plan options offered under the product?

What are the Entry Age / Maturity Age criteria?

What is the minimum and maximum Policy Term?

What are the criteria for Sum Assured?

Minimum Basic Sum Assured: ` 20, 00,000.

The Basic Sum Assured can be selected in multiples of ` 1, 00,000 only. There is no upper limit for the Basic Sum Assured. What is the premium criteria?

The minimum premium (exclusive of Service Tax) is ` 3,500 for all plan options.

The premium can be paid only in annual mode. There is no upper limit. Why should I buy SBI Life - eShield?

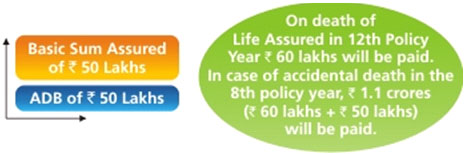

Why should I opt for Accidental Death Benefit?

What are the different Plan options available and the Death Benefit offered under each of them?

What are the premium payment modes available?

The Premiums can be paid in annual mode only.

Can the Nominee be a Minor?

Yes, a Nominee can be a Minor.

However, an Appointee (major) has to be provided for the Minor Nominee. What will the beneficiary get in case the insured commits suicide?

If the life assured commits suicide within one year from the risk commencement date,

whether sane or insane at that time, the nominee will be entitled to 80% of the

premiums paid, provided the policy is in force, the policy will be void and no claim

will be payable.

If the life assured commits suicide within one year from the reinstatement date if reinstated, whether sane or insane at that time, the nominee will be entitled to 80% of the premiums paid till the date of death, the policy will be void and no claim will be payable. The premium to be considered for the purpose would be the base premium only. Service tax, cess, Accidental Death Benefit premium and extra premiums, if any, would not be considered for refund What are the benefits of opting for a higher Sum Assured?

What is the Grace Period under the product?

A Grace Period of 30 days from the premium due date will be allowed under the product.

Can a loan be taken under this product?

Loan is not available under this product.

What are the tax benefits available?

Tax deduction under Section 80C is available. However in case the premium paid during

the financial year, exceeds 10% of the Sum Assured, the benefit will be limited

up to 10% of the Sum Assured.

Tax exemption under Section 10(10D) is available, subject to premium not exceeding 10% of the Sum Assured in any of the years during the term of the policy. Tax benefits, are as per the Income Tax laws & are subject to change from time to time. Please consult your tax advisor for details. As an NRI, can I buy life insurance under SBI Life - eShield?

SBI Life - eShield is only for resident citizens of India. However, we have other

plans (including term plans) which can be purchased through insurance advisors,

distributors or the State Bank Group bank branches by NRIs. We would be glad if

you could provide us your details and our representative will be happy to guide

you through the purchase of those plans. You can write to us at buyonline@sbilife.co.in.

Can I insure my spouse / children?

No. You can only insure yourself in this plan. However, it is mandatory that the

Life Assured has to be over 18 years.

Can I get term insurance cover if I am a smoker or use tobacco in any form?

Yes. However, smoker rates are higher than the non-smoker rates. A person is considered

as a non-smoker if he/she has not been smoking or using tobacco in any form for

at least last 5 years.

When will my life insurance cover begin?

Your coverage will begin only on acceptance of your proposal form. A written confirmation

would be sent to you in this regard.

Can I take a print out of the Online Form and make a cheque payment at any SBI Life branch?

SBI Life - eShield is offered Online only. You can only pay through Debit / Credit

card or through Internet Banking mode.

If you wish to take the policy through cheque payment (offline mode), there are other plans which can be purchased through our insurance advisors, distributors or the State Bank Group bank branches. We would be glad if you could provide us your details and our representative will be happy to guide you through the purchase of those plans. You can write to us at buyonline@sbilife.co.in. What is Underwriting?

During underwriting we evaluate your proposal. The evaluation is based on the information

submitted by you in the proposal form and the results of your life insurance medical

examination. Term insurance underwriting generally takes 3-4 days once all the requirements,

such as insurance medical examination, financial and other related documents, related

to your insurance proposal are received by us.

What are the conditions for reviving the policy?

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||